What Are Exogenous Variables?

Exogenous variables or external factors are crucial in time series forecasting as they provide additional information that might influence the prediction. These variables could include holiday markers, marketing spending, weather data, or any other external data that correlate with the time series data you are forecasting. For example, if you’re forecasting ice cream sales, temperature data could serve as a useful exogenous variable. On hotter days, ice cream sales may increase.How to Use Exogenous Variables

Step 1: Import Packages

Import the required libraries and initialize the Nixtla client.Step 2: Load Dataset

In this tutorial, we’ll predict day-ahead electricity prices. The dataset contains:- Hourly electricity prices (

y) from various markets (identified byunique_id) - Exogenous variables (

Exogenous1today_6)

| unique_id | ds | y | Exogenous1 | Exogenous2 | day_0 | day_1 | day_2 | day_3 | day_4 | day_5 | day_6 |

|---|---|---|---|---|---|---|---|---|---|---|---|

| BE | 2016-10-22 00:00:00 | 70.00 | 57253.0 | 49593.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 1.0 | 0.0 |

| BE | 2016-10-22 01:00:00 | 37.10 | 51887.0 | 46073.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 1.0 | 0.0 |

| BE | 2016-10-22 02:00:00 | 37.10 | 51896.0 | 44927.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 1.0 | 0.0 |

| BE | 2016-10-22 03:00:00 | 44.75 | 48428.0 | 44483.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 1.0 | 0.0 |

| BE | 2016-10-22 04:00:00 | 37.10 | 46721.0 | 44338.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 1.0 | 0.0 |

Step 3: Forecast without Exogenous Variables

First, let’s create a baseline forecast without using any exogenous variables.Step 4: Forecasting with Exogenous Variables

Next, let’s create a forecast using the exogenous variables. To make a forecast using exogenous variables, you need to provide historical and future exogenous values. Below is an example dataset containing future exogenous variables. Note that it only contains the future exogenous variable values not the target variabley. We need to forecast this target variable using the exogenous

variables provided.

| unique_id | ds | Exogenous1 | Exogenous2 | day_0 | day_1 | day_2 | day_3 | day_4 | day_5 | day_6 |

|---|---|---|---|---|---|---|---|---|---|---|

| BE | 2016-12-31 00:00:00 | 70318.0 | 64108.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 1.0 | 0.0 |

| BE | 2016-12-31 01:00:00 | 67898.0 | 62492.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 1.0 | 0.0 |

| BE | 2016-12-31 02:00:00 | 68379.0 | 61571.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 1.0 | 0.0 |

| BE | 2016-12-31 03:00:00 | 64972.0 | 60381.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 1.0 | 0.0 |

| BE | 2016-12-31 04:00:00 | 62900.0 | 60298.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 1.0 | 0.0 |

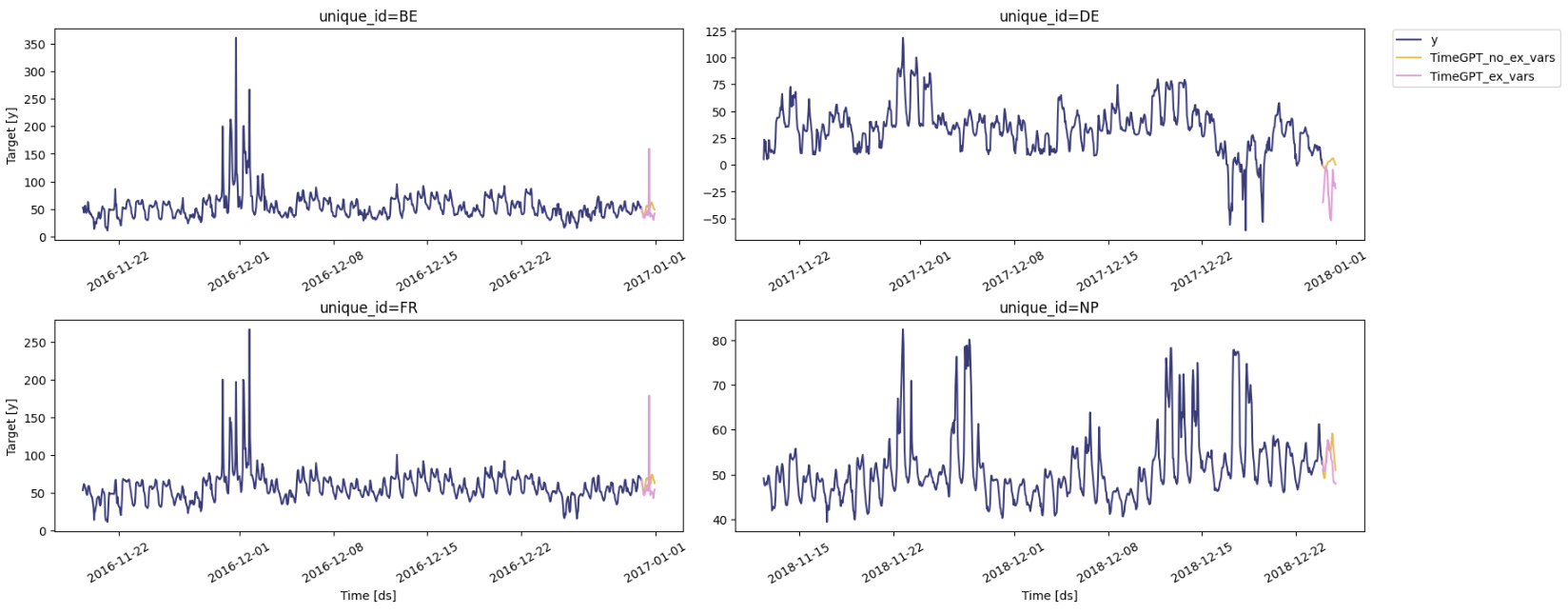

Step 5: Forecast Visualization

Once you have generated your forecasts, you can visualize the results to compare forecasts between the two methods above.

Key Takeaways

- Exogenous variables enrich time series forecasting.

- Ensure proper alignment of historical and future exogenous data.

Next Steps

Congratulations! You have mastered the fundamentals of adding exogenous variables to your TimeGPT forecasts. Keep refining your approach by- Exploring feature engineering to create domain-specific exogenous data.

- Experimenting with different modeling approaches for external variables.

- Validating forecast accuracy by comparing with real future data.